No-Till Farmer

Get full access NOW to the most comprehensive, powerful and easy-to-use online resource for no-tillage practices. Just one good idea will pay for your subscription hundreds of times over.

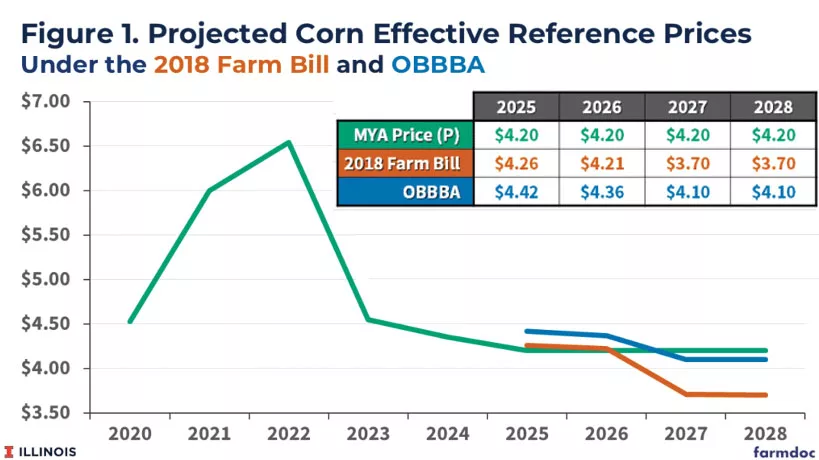

PAYING MORE. Effective reference prices under OBBBA will be higher than those had in the 2018 Farm Bill, primarily because of the higher statutory reference prices. farmdoc

Although growers will face plenty of uncertainty in the 2026 growing season with grain prices, input costs and interest rates, the One Big Beautiful Bill Act passed by Congress last year will provide some significant benefits in the future.

Advocates of the legislation believe it will lower the cost of borrowing for America’s farmers, reduce the tax burden on interest income for loans secured by real property for agricultural production, and lower the administrative burden for small farmers and ranchers employing temporary and seasonal workers.

One immediate change is the permanent 100% bonus depreciation for new equipment purchased after Jan. 19, 2025, and the Section 179 deduction is increased to $2.5 million (with a $4 million threshold). This allows for immediate, full write-offs for farm machinery and capital improvements, plus offering a 20% Qualified Business Income Deduction (QBID) and higher estate tax exemptions.

These changes reverse prior phase-outs, making it easier for farms to expense large purchases like tractors and combines in the year bought, rather than depreciating them over many years.

Instead of spreading costs (for example, a $500,000 combine) over years, farmers can deduct the full amount in the year of purchase. This could make expensive machinery, barns and land improvements more accessible by reducing the immediate tax burden.

The estate tax exemption is significantly raised to $15 million per individual, or $30 million per couple, plus inflation adjustments, protecting more family farms from the so-called “death tax.”

Passage of the…

Get full access NOW to the most comprehensive, powerful and easy-to-use online resource for no-tillage practices. Just one good idea will pay for your subscription hundreds of times over.

Download these helpful knowledge building tools

We have engineered and developed the most advanced concave system that threshes all crops, eliminates rotor loss, improves grain quality, gives you a cleaner sample – all with one set of XPR concaves.

At Titan International, our product portfolio reflects our commitment to innovation and high-quality products. Titan International offers a full line of solution-focused wheel, tire, and undercarriage products for a wide variety of off-the-road equipment in agriculture, construction, forestry, mining, power sports, high-speed trailers, and outdoor power equipment segments. As one of the largest North American manufacturers, with a network of dealers all over the world, Titan is an industry leader that original equipment manufacturers and operators can count on for durable products and quality service.

Provide expert analysis and decision support to increase productivity and profitability.