Running a large-scale farm and cattle operation involves more than caring for the land and animals. It is a business operation that requires sound financial records so that decision making can be based on data rather than emotion.

Brian Pine, a field analyst with K·Coe Isom, a consulting firm based in Kansas that helps sustain and grow ag operations in fluctuating conditions such as weather, commodity price volatility, land values and economic pressures, is working with a producer in Kansas to get a better handle on his finances. When it comes to the business strategies of the farm, the producer is conservative. “This client’s concern is that his farming operation has grown to the point where his legal pad, and random spreadsheets used to track his finances just doesn’t cut it anymore,” Pine explains.

Case Study Scenario

Five years ago this Kansas farmer and his wife took over the row-crop and cattle operation from his parents, who had started farming 50 years ago. When he returned to the farm 25 years ago, the operation underwent significant growth in order to financially support the two families — his and his parents’. The operation grew both by buying and renting more acreage and expanding the cattle herd.

“It then settled out into a more methodical growth rate while they focused their attention on debt servicing,” explains Pine, who serves as a consultant for the farmer. “Ten years ago they began seeing additional opportunities for growth in both the row-crop and cattle operations.”

Today, the operation has 3,800 total acres of row crops. Of that, they own 24%, cash rent 8% and share crop 68%. The farm has become more diversified, growing both irrigated and dryland corn, soybeans, milo, silage, brome hay and prairie hay. The 1,227 head livestock operation includes a cow-calf herd, backgrounding and finishing cattle.

Operation at a Glance

Location: Kansas

Operation: Corn, soybeans, double cropped soybeans, milo, wheat, double crop milo, silage, brome hay, prairie hay, cow-calf, backgrounding cattle and finishing cattle

Total Acres: 3,800

Total Cattle: 1,227

Employees: 6

Average Annual Revenue: $1,802,000

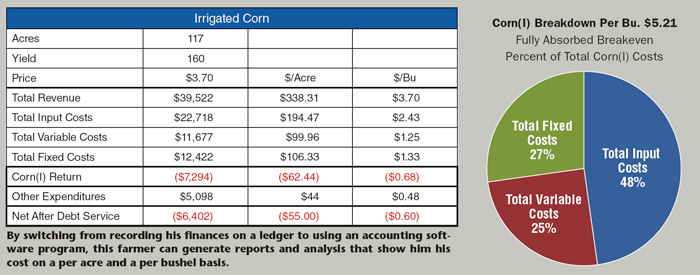

By switching from recording his finances on a ledger to using an accounting software program, this farmer can generate reports and analysis that show him his cost on a per acre and a per bushel basis.

Growing Challenges

Like many of his peers, this farmer had been doing most of his bookkeeping via ledgers and basic spreadsheets. “Unfortunately, this is often the case until the farm’s financial responsibilities get to a size that the previous way of managing their finances is no longer effective,” explains Dennis Roddy, a manager with K·Coe Isom and a former agricultural loan officer. It’s not uncommon, he adds, for farmers to gauge their success simply by how much money is in their checking account, or by how much money the bank is willing to loan them.

While this farmer was using spreadsheets to keep track of some data, Pine says he wasn’t taking into account all associated expenses, such as living expenses. They also were not connected back to the rest of the business to give him a CFO level look at his operation. “It was segmented in that he might have one spreadsheet to track input costs and another to track a load of 550 pound calves on,” he says. Nothing took into account such things as his overhead expenses or debt servicing. Thus, he was not able to perform detailed analysis by profit center in a way that would allow him to make sound business decisions.”

According to Pine, the farmer acknowledged the need for better financial tracking and understanding. “He said, ‘Brian, I just feel like this thing is getting out of control. I’ve been fortunate so far because I’m pretty conservative, but I couldn’t tell you exactly what my cost of production is for an acre of corn or for a weaned calf. That’s not good when I’ve got this many dollars running through my operation. I need to have a better handle as to what’s going on and I’d like to be able to sleep a little better at night, knowing that I understand my finances.’”

Recognizing he has the opportunity for more growth in coming years, both in crop farming and cattle, the farmer was willing to make the changes that would enable him to take advantage of those opportunities. Pine says that this thirst for knowledge is one of his biggest strengths and is what will help him successfully grow his operation.

Professional Consultant’s View

The farmer enlisted K·Coe Isom to help build a budget, manage his cash flow, and generate useable reports for decision making. Before they could begin to understand the farmer’s cost of production, cost per acre, return on assets, and other important metrics, the data needed to be better organized. One of the operation’s most significant weaknesses is that the farmer had “virtually no set accounting system in place,” Pine says.

He recommended first establishing a budget by class so each profit center (each individual crop and livestock operation) could be evaluated individually. This would help him understand the potential flow of funds in and out of his operation. Then, he could improve costs and efficiencies by setting up a system that generates key reports to drill into the financial data to begin managing vs. reacting to changes in the business.

“By doing so, he will understand his cost of production by profit center; giving him a level of detail he has only guessed at before — whether it’s the true cost of a weaned calf or profit on irrigated vs. dryland corn and the true return on his pivots.

“This will do many things for him,” Pine explains. “It’s not only informational and essential to know, but more importantly, it’s going to help him be a more effective marketer as he’ll know his fully absorbed breakevens for all profit centers. As the markets change throughout the year, he’s not going to be blindly selling at random prices just because the market has gone up.”

Compiling Data

But before they could get to that point, a lot of data gathering was needed.

“For us to do a good job, we have to have detailed financial information.

We had to become intimate with his finances,” Pine explains. “We see this frequently — not just with this operation — the process of gathering accurate, detailed financial information can be a steep learning curve in and of itself.”

As an example of the detailed information needed, clients are asked for input invoices by crop. “Typically they’ll give us one big bill from the co-op that has seed, chemical and fertilizer all bundled together,” he says. “The deeper you go, the more challenging it can become for the producer. This exercise generally leads the operator to realize how much of a void there is in his/her true financial understanding of the operation.”

A task like this helps the farmer better grasp the level of detail needed to produce accurate financial reports such as breakeven cost of production. “We try to explain to clients ahead of time that it is a challenging process. The big misconception is that we have a magic wand that we can wave over their finances and magically tell them what their cost of production is. It is a joint effort,” Pine explains.

Recording and organizing the amount of detail needed can be time consuming and difficult. With this particular case there will be the added challenge of learning new technology since the farmer, while tech-savvy when it comes to his equipment, hasn’t dealt with any type of financial software previously.

Pine and the farmer went through all of the operation’s 2014 numbers. “In the ideal world, it would be nice to have 3 years of history to work from, but it was going to take more time than it was worth to go back and try to make heads or tails of his records. We just needed to start somewhere to establish our initial budget.”

Another Take on ‘Sustainability’

Sustainability, particularly as it relates to farming, means something different to everyone you ask. K·Coe Isom uses the term in reference to the farming operation as a business.

“As our firm discusses it and as we try to get farmers to understand it — sustainability for them came down to creating something that’s long lasting — setting up the right systems and the right processes so that the family farm is here for the long haul,” explains Marc Johnson, a principal with K·Coe Isom.

“This kind of thought process is starting to get out there where a farmer who is in his second or third generation is starting to understand that he’s already beat the odds,” Johnson says. “Now asking, ‘How do I not screw this up so I can also transition to the next generation or successfully monetize my family’s long term investment in it.’”

The ‘Ah-Ha’ Moment

The first meeting after gathering the data from 2014 and establishing a 2015 budget and cashflow produced a number of ‘ah-ha’ moments for the farmer.

“By the end of the meeting our client said, ‘We need to go ahead and fast track this accounting software deal. There’s no decision to make other than which package we are going to use. How quickly can you help us get set up and trained?’” Pine says.

The information gathering process can be tedious and is an added time constraint farmers get concerned about, but at the end of the day they’re happy they did. “When we come back to them with the information and all of a sudden they sit there and say, ‘Now this is information I can utilize to help make daily decisions and future plans. I never knew my true cost of production on an acre of corn or a weaned calf or that my labor costs had this much impact on my breakevens. This client’s comment to us was, ‘Your firm now knows more about my finances than I do.’”

The farmer found having someone else know as much or more about his finances than him to be a bit disconcerting. It was also reassuring to have a trusted business partner who understands the data and could help him figure it out.

That reassurance really eased much of the farmer’s concerns. After that first big meeting, he told Pine, ‘Let’s just go ahead and do the whole system. Let’s get it going as quickly as possible; I can see where this is heading. This is what we’ve been missing for a long time.”

The use of a system that not only produces budgets and reports, but interacts with professional analysts, helps to ensure that focus is given to the finances of the business proactively throughout the year, not just reactively at year-end for a limited focus on tax savings, Pine says.

3 Homework Questions

Brian Pine, field analyst with K-Coe Isom based in Lenexa, Kan., says if he was a farmer who wanted to get a better handle on his financial reports and cost of production, three of the most important questions he would pose include these:

1.What does “fully absorbed breakeven” mean?

2. How long of a process is the initial set up?

3. How do I know if I need this kind of assistance?

Click here for the expert’s responses to these three questions.

Improving the Operation

When a farmer is better able to understand his costs of production — particularly when it comes to crops — he can start correlating that information to many management decisions — what type of crop insurance coverage he needs, what costs are out of key industry performance ranges, how many employees are actually needed, and the list goes on and on.

The recommended system would allow for easy breakdown by profit center, into mini budgets. “It helps the farmer to understand his variable costs, fixed costs, capital costs, and other metrics defined in the reports. If he wants to look at labor costs, he will not only understand it as a lump sum, but he can dive deeper to understand it in terms of dollars per acre, dollars per bushel, dollars per labor hour, and understand each as a percentage of your total costs. This will allow him to quickly identify his big opportunities on the expense side,” Pine says.

Refining Lease Terms

In this particular case, it brought to light rather quickly that the farmer’s rental arrangements needed some attention. “We don’t have the final answer yet for him, but it is one of our top priorities. We will do some different analyses for him to help him understand what it’s going to take to get the arrangements to a profitable point and then help him develop an approach to negotiate with his landlord,” Pine says.

Once this farmer has a stronger grasp of his operations, he’ll be able to go to his landlord and point to his strengths and weaknesses. “He can say, ‘Here are my numbers, and yes I can fix that. I’ve already talked to my guys about this. Here are the things I’m fixing to make that better. So, you’re not going to have to pay for that or risk that as the landlord. I’m going to get that under control. But here’s one thing that I can’t get under control — my lease arrangements. And here’s what the industry data says and how I compare.’

“Essentially, the power of this information is that it gives our producers a logical, mathematical, financial, emotionless decision making tool,” Pine says. And, that will help him and his landlords adjust the leases accordingly to everyone’s benefit.

“He’s going to understand his cost of production by profit center; giving him a level of detail he has only guessed at before…”

Pine says the frequency of how often leases are reviewed has changed in the last few years. “When I farmed, it was not unusual for us to look at leases once every 5 or 10 years. Typically, we’d have a 5-year lease that automatically re-upped as long as no one desired a change. So really, they were reviewed once every 10 years. With the fluctuation in markets, the rapid rise in production costs over the last few years, and the competitive nature of the industry, we’re seeing rental arrangements being addressed or tweaked, if not every year, at least every other year.”

Improving Purchasing

Roddy adds, “Understanding this information is the first step. The next is using it to help make every decision. So, if a section of land comes up for auction near them — and land doesn’t come up for auction around here very often — the emotional response is, ‘I’ve got to buy that at all costs.’ This will then push up the price and forces the farmer to take on more debt.”

Roddy offers this example. With this farmer, if some non-irrigated land became available, but he knew that financially he could not take on any more non-irrigated land and maintain his budget goals, he can make the decision based on facts, and not emotion.

“He’s able to look at the situation and say, ‘Well, I realize that land is out there, but if I’m going to buy it, here’s the max debt load I can take on.’ This takes the emotion out of the decision and he buys it only if it makes sense. It’s the same with the equipment, bringing on a new employee or expanding the cattle herd. All of those decisions are now driven by facts.”

The goal for this farmer is to make his decision-making processes easier and to enable him to make solid decisions that make the most financial sense for his business. “What we told the client is this: when you really know your numbers, and have meaningful, useable reports based on solid financial data, you will trust it and are willing to follow it, then your batting average is going to go up. It doesn’t mean you’re going to get every decision right. You may not like the decision you have to make, but the process of making it becomes easier.”

Making decisions based on sound financial data is critical in running any kind of a business. But this can be a very new concept to a family farm accustomed to emotional decision making .

The Next Step

Meet the Expert

Brian Pine

K-Coe Isom

Kansas City, Kan.

913-643-5000

bpine@kcoe.com

Brian Pine is a field analyst with K·Coe Isom in its AgKnowledge division and is based in the firm’s Kansas City office. His business footprint extends from Kansas into the Corn Belt. He joined the firm in 2014 after spending more than 20 years helping to manage his family’s farm — Pine Family Farms and Pine Family Landscape. During his time in the family business, Pine had the opportunity to participate in all aspects of the business, including managing partner duties. He has a bachelor’s degree in agribusiness from Kansas State University. Pine Family Farms has been a client of K·Coe Isom for over 25 years.

While some issues, such as the lease agreements, have already come to light, Pine says the next step is to start doing some year-over-year trends for the farmer. “We can do ratio analysis and other things that will give him even more information about his business that he can then use to help make decisions moving forward.”

With the amount of money this farmer owes the bank and his annual gross revenues, some businesses would have a CFO in place to take care of his financial analysis, Roddy says. But, the farmer will never get to the point where it makes sense or be willing to hand over the kind of money needed to pay a CFO. “So we become that CFO for him. We’ve already got the data in place. We can start giving him this CFO-level analysis immediately without the recurring payroll or lengthy training process.”

Once the farmer and his wife are set up with a financial software system, K·Coe Isom will assume a training program on its use, in particular with the wife who will be overseeing data entry. “For the rest of the year we’ll be producing budget-to-actual reports for him on a monthly basis, so that we can see how things are really going compared to what we projected,” Pine says.

In the first year it’s typical to see a lot of variance in the budgets because the initial data is rarely perfect, Pine says. Now that all of the 2014 data is entered and the 2015 information is gathered Pine will begin working with the farmer to build his 2016 and beyond budget.

Web Exclusive: Expert Responses

Click below to view other case studies from this report: